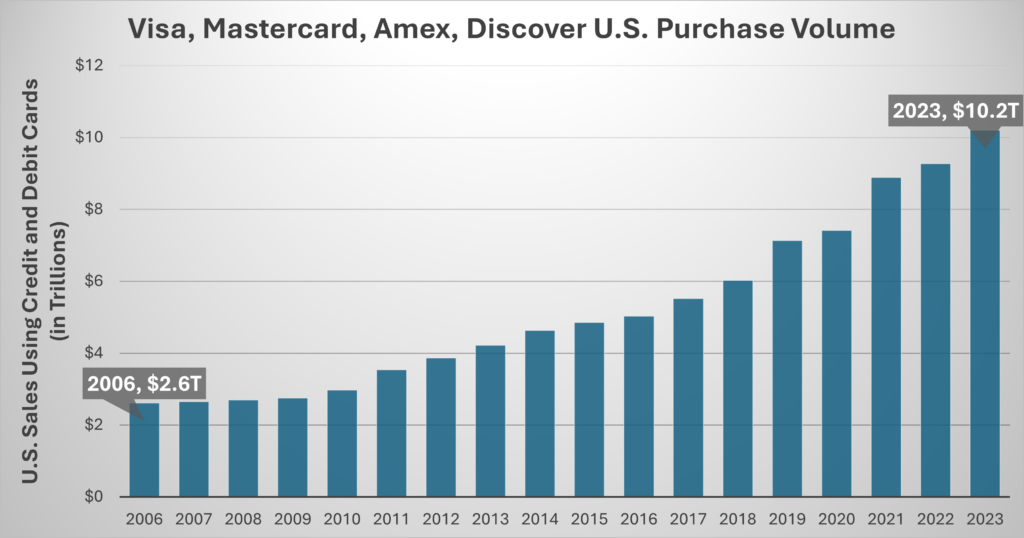

WASHINGTON, DC – Sales through credit and debit card transactions have driven more than $93 trillion in economic activity since 2006, according to purchase volume data from Nilson.

“Credit and debit card payments are fueling our nation’s economy,” said Electronic Payments Coalition Executive Chairman Richard Hunt. “Consumers prefer to pay with cards because of the convenience, built-in security protections and popular cashback reward programs, which families use to help fight rising inflationary prices. For businesses of all sizes, card transactions provide secure, timely payments. The leading processing networks invest billions into protecting consumers and the safety of our global payment networks. And, despite these investments, credit card processing costs have remained virtually flat for nearly a decade and are significantly cheaper than the cost associated with processing cash.”

In a recent legal filing, the Office of the Comptroller of the Currency wrote, “Credit and debit card transactions help to propel the Nation’s economy by facilitating commerce.”

The IHL Group, a retail advisory firm, found accepting and processing cash has a substantial cost of at least 4.7% for businesses and more for some retail segments. Credit card processing, on the other hand, is about 2% and capped for debit cards.

In addition to more than $93 trillion in economic activity, accepting credit and debit cards saved businesses a minimum of $2.35 trillion since 2006 when compared to the equivalent in all-cash transactions.

Some politicians and special interest groups are ignoring the facts to push legislation placing new mandates on Americans’ credit cards. The Durbin-Marshall Credit Card Bill would require credit cards to have the ability to run on secondary, untested networks. This change would lead to increased fraud and threaten valuable rewards programs.

Supporters of the legislation claim the proposed mandates would lead to lower costs for consumers but the independent Congressional Research Service examined the Durbin-Marshall Credit Card Bill and concluded “it is not clear whether retailers would pass interchange savings on to consumers.” Additionally, the Federal Reserve Bank of Richmond found 98% of retailers either raised prices or kept them the same following government price caps on debit card processing costs.

“It just doesn’t make sense when you look at the facts,” Hunt said. “D.C. politicians and their campaign donors are trying to build a narrative that does not exist in order to pass a law that hurts small businesses and consumers so the largest corporate mega-stores can have another windfall.

“Instead of trying to find a problem that doesn’t exist, the supporters of Durbin-Marshall should ask corporate mega-stores why they have continued to raise prices on consumers despite credit card processing costs having remained flat for a decade.”