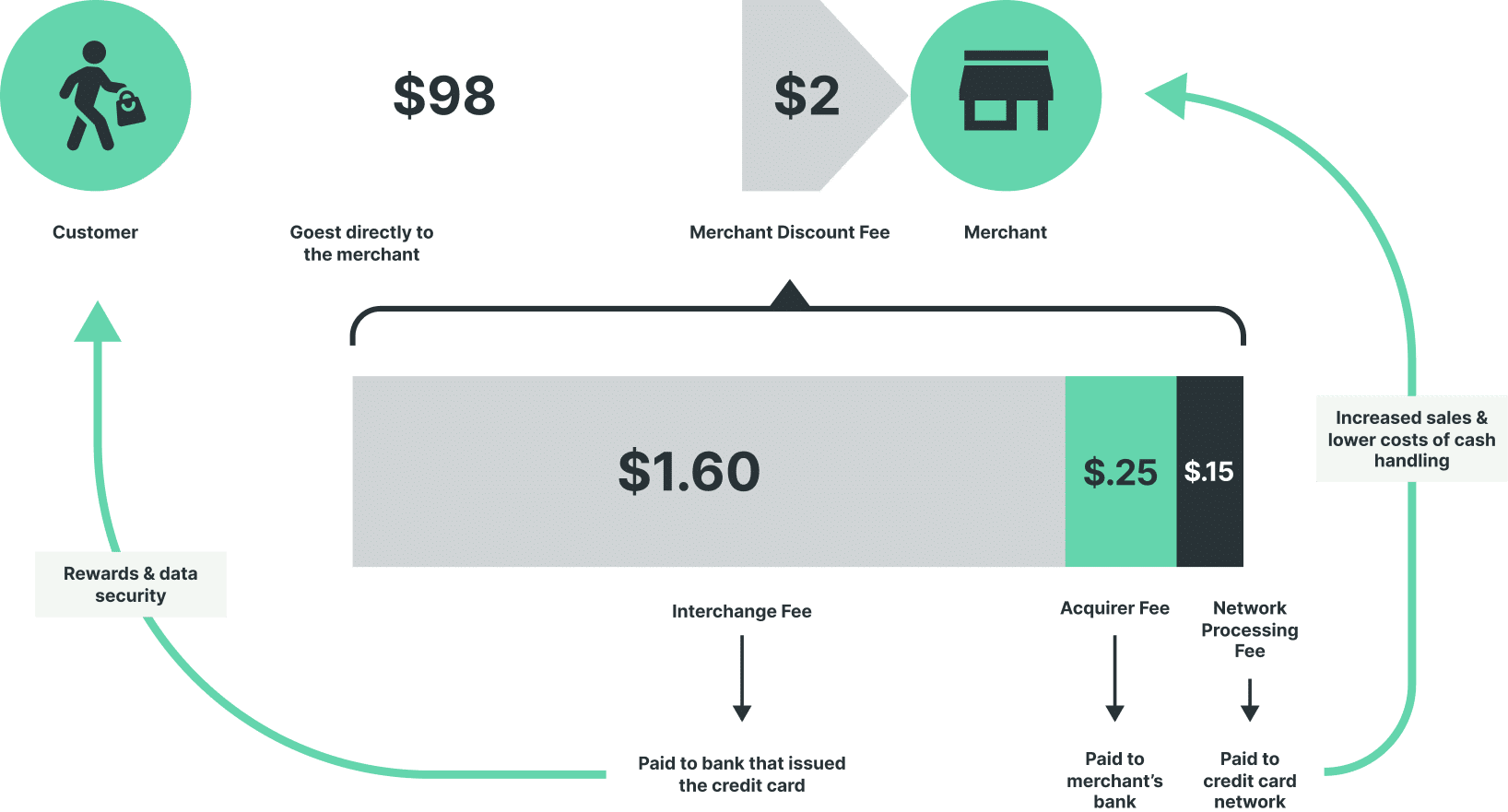

Credit cards provide consumers with a fast, secure, and convenient way to pay, along with fraud protection, zero-liability guarantees, data privacy, access to credit, and rewards programs. These benefits all require significant investment in customer service, fraud detection, secure technology, and chargeback systems.

Interchange helps cover those costs and enables ongoing investments in innovation to ensure the nation’s electronic payments ecosystem remains secure, rewarding, and resilient to threats.

The result is a system that benefits everyone: consumers enjoy security, speed, and rewards, while businesses gain access to a trusted, reliable, and globally connected network, essential in today’s digital economy.

Why Credit Cards Matter

How Interchange Supports the System

A System That Benefits Everyone